- UBS AG

- Credit Suisse AG, Credit Suisse Fides, and Clariden Leu Ltd.

- Wegelin & Co.

- Liechtensteinische Landesbank AG

- Zurcher Kantonalbank

- swisspartners Investment Network AG, swisspartners Wealth Management AG, swisspartners Insurance Company SPC Ltd., and swisspartners Versicherung AG

- CIBC FirstCaribbean International Bank Limited, its predecessors, subsidiaries, and affiliates

- Stanford International Bank, Ltd., Stanford Group Company, and Stanford Trust Company, Ltd.

- The Hong Kong and Shanghai Banking Corporation Limited in India (HSBC India)

- The Bank of N.T. Butterfield & Son Limited (also known as Butterfield Bank and Bank of Butterfield), its predecessors, subsidiaries, and affiliates

- Sovereign Management & Legal, Ltd., its predecessors, subsidiaries, and affiliates (effective 12/19/14)

- Bank Leumi le-Israel B.M., The Bank Leumi le-Israel Trust Company Ltd, Bank Leumi (Luxembourg) S.A., Leumi Private Bank S.A., and Bank Leumi USA (effective 12/22/14)

30 December 2014

USA: IRS - Foreign Financial Institutions or Facilitators

29 December 2014

Treaty Shopping Involving South Africa Tax Treaty with Mauritius

South African investors have used Mauritius as a vehicle for investing in other countries with which Mauritius has treaties. Likewise, international investors from other countries that have tax treaties with Mauritius have used Mauritius as an intermediary to invest in South Africa.

The first tax treaty between South Africa and Mauritius came into force in 1960, through the South Africa/United Kingdom tax treaty, which was extended to Mauritius. During that time, Mauritius was still a colony of the United Kingdom. It is important to note that even though Mauritius gained its independence from the UK in 1968, the above-mentioned tax treaty was still applicable to Mauritius until termination in 1997 with the coming into force of a new tax treaty in 1997 directly between South Africa and Mauritius. However South Africa signed a new treaty with Mauritius on 17 May 2013. The South African Parliament ratified the treaty on 10 October 2013. The treaty must similarly be ratified by Mauritian Authorities. Thereafter it has to be published in the Government Gazette in terms of section 108 of the Income Tax Act No 58 of 1962 (Act).

The main reason for the signing a new the treaty (hence forth “draft treaty”) was due to perceived “abuse” of the 1997 tax treaty and resultant erosion of the South African tax base. The World Bank and the International Finance Corporation have consistently ranked Mauritius as one of the best Sub-Saharan African countries in which to do business. The main drivers are that Mauritius:

- Is a member of SADC, WTO and COMESA.

- Has a vast network of treaties with countries. It is party to 35 double taxation agreements.

- has no capital gains tax.

- has a low corporate income tax rate at 15%, which translates into an effective tax rate of 3% after taking into account available credits. (GBL1 gets up 80% credit while GBL2 qualifies for exemption).

The Mauritius/India Tax Treaty – Sale of Shares Taxable only in Shareholder Country

South African residents wishing to invest in India often take advantage of the Mauritius/India treaty by routing investments via Mauritius in order to gain tax advantages. In terms of the South Africa/India treaty (and most other treaties with India) capital gains derived from the sale of shares in a company may be taxed in the country in which the company whose shares are being sold is a resident (i.e. in India), and since India has a tax on capital gains the gain does not escape taxation. In short, where a South African company invests directly into India it will be subject to CGT on the sale of the shares in the Indian company. To avoid such taxation, South African investors route investments via Mauritius by setting up a GB1 company in Mauritius which takes advantage of the provisions in the Mauritius/India treaty, which provides that capital gains arising from the sale of shares are taxable only in the country of residence of the shareholder and not in the country of residence of the company whose shares are being sold. As a result, a company resident in Mauritius selling shares of an Indian company will not pay tax in India on the disposal of the Indian company’s shares. Since there is no capital gains tax in Mauritius, the gain will escape tax altogether. The capital gain can then be repatriated back to the South African shareholder free of withholding taxes as Mauritius does not levy tax on dividends, interest or royalties for GBL1 companies.

Mauritius/African Tax Treaty Network – Lower Withholding Tax Rates

South African companies often route investments into other Africa countries via Mauritius since Mauritius has negotiated better benefits in its tax treaties with some African countries than South Africa has. This is especially so with regard to withholding tax rates (on dividends, interest, royalties and management/technical fees) in treaties between Mauritius and other African countries, which are generally lower than the withholding tax rates in tax treaties between South Africa and other African countries. To take advantage of the treaties that Mauritius has signed with some African countries, investors will route their investments in Africa via Mauritius.

Mauritius Seen Favoring Ex-Central Bank Head to Reoccupy Post

A former central bank governor and an ex-chairman of the stock exchange commission have emerged as possible frontrunners to replace Bank of Mauritius Governor Rundheersing Bheenick, who was fired last week.

27 December 2014

New Mauritius government sacks long-serving central bank governor

Mauritius central bank governor on Saturday said he had been sacked by the Indian Ocean island's new government after seven years in charge of the bank, but hinted that he may appeal the move.

26 December 2014

FSC Mauritius releases Annual Report 2013

The Financial Services Commission, Mauritius (FSC Mauritius) is required under Section 85 of the Financial Services Act 2007 to report on its activities together with its audited financial statements in respect of the previous financial year (The Annual Report).

The FSC Mauritius is pleased to announce the release of its Annual Report 2013.

The Annual Report 2013 was laid before the National Assembly on Monday 22 December 2014.

23 December 2014

Jersey Finance CEO explores role of IFCs in developing countries at roundtable event

Jersey Finance CEO Geoff Cook has taken part in a roundtable discussion to explore the relationship between international finance centres and developing countries.

The Government of Jersey event took place on 26 November in London and follows the publication of the Jersey’s Value to Africa report, launched in association with Chatham House, earlier that month.

Read more about the roundtable event in The House

19 December 2014

USA: Court Authorizes Internal Revenue Service to Issue Summonses For Records Relating To U.S. Taxpayers Who Used Services of Sovereign Management & Legal Ltd. to Conceal Offshore Accounts, Assets or Entities

Deputy Assistant Attorney General David Hubbert for the Justice Department’s Tax Division Civil Trial Matters, U.S. Attorney Preet Bharara for the Southern District of New York, Commissioner John Koskinen of the Internal Revenue Service (IRS), and Special Agent in Charge Anthony D. Williams of the Drug Enforcement Administration’s (DEA) Los Angeles Field Division announced that U.S. District Judge Vernon S. Broderick entered an order yesterday authorizing the IRS to issue summonses requiring Federal Express Corporation, doing business as FedEx Express, FedEx Ground Package System Inc., aka FedEx Ground, DHL Express (DHL), United Parcel Service Inc. (UPS), Western Union Financial Services Inc., the Federal Reserve Bank of New York (the FRBNY), Clearing House Payments Company LLC, and HSBC Bank USA National Association (HSBC USA) to produce information about U.S. taxpayers who may be evading or have evaded federal taxes by using the services of Sovereign Management & Legal Ltd. (Sovereign) to establish, maintain or conceal foreign accounts, assets and entities.

In this action, the court granted the IRS permission to serve what are known as “John Doe” summonses on FedEx Express, FedEx Ground, DHL, UPS, Western Union, the FRBNY, Clearing House and HSBC USA. The IRS uses John Doe summonses to obtain information about possible tax fraud by individuals whose identities are unknown. The John Doe summonses direct these eight entities to produce records that will assist the IRS in identifying U.S. taxpayers who, from 2005 through 2013, used Sovereign’s services to establish, maintain, operate or control any foreign financial account or other assets; any foreign corporation, company, trust, foundation or other legal entity; or any foreign or domestic financial account in the name of such foreign entity.

“This summons action is but the latest step in the Department of Justice’s efforts to identify and hold fully accountable U.S. taxpayers who have sidestepped their tax obligations by hiding money overseas,” said Deputy Assistant Attorney General Hubbert. “The world is getting smaller for tax cheats, and we will work with our partners at the IRS to vigorously enforce the nation’s tax laws against those who seek to avoid paying their fair share.”

“This action demonstrates our Office’s commitment to pursuing tax evaders who use offshore service providers to avoid their U.S. tax obligations,” said U.S. Attorney Bharara. “By issuing these John Doe summonses, we continue our joint efforts with the IRS to identify and hold accountable those who conceal their foreign assets in order to dodge their legal responsibility to pay taxes.”

“The IRS remains committed to continuing our priority efforts to stop offshore tax evasion wherever it is found,” said Commissioner Koskinen. “We have made tremendous progress in this area, working cooperatively with other agencies. The John Doe summons remains an important tool in our efforts to find international tax evaders and those who help them.”

“The DEA has a longstanding commitment to sharing information with our federal, state, and local partners,” said Special Agent in Charge Anthony D. Williams. “Issuance of these summonses exemplifies how outstanding investigative results can be derived from a culture of interagency cooperation.”

According to the allegations set forth in the documents filed in support of the petition, and other information in the public record:

Sovereign is a multi-jurisdictional offshore services provider that offers clients, among other things, the formation and administration of anonymous corporations and foundations in Panama as well as offshore entities. Related services provided by Sovereign include the maintenance and operation of offshore structures, mail forwarding, the availability of virtual offices, re-invoicing, and the provision of professional managers who appoint themselves directors of the client’s entity while the client maintains ultimate control over the assets.

As a result of a DEA investigation of online narcotics trafficking known as Operation Adam Bomb, the IRS learned that Sovereign was involved in assisting U.S. clients evade their taxes. During the IRS investigation that led to today’s action, one taxpayer, making a voluntary disclosure of tax non-compliance to avoid prosecution, reported that Sovereign helped the taxpayer form an anonymous corporation in Panama that the taxpayer used to control assets without appearing to own them.

The IRS investigation also determined that Sovereign uses Federal Express, UPS and DHL to correspond with U.S. clients, and Western Union to transmit funds to and from clients in the United States. In addition, the IRS learned that the wire services operated by the FRBNY and Clearing House, and the U.S. correspondent bank accounts that HSBC USA holds for Sovereign’s banks in Panama and Hong Kong, are likely to have records of financial transactions between Sovereign and its clients in the United States. By obtaining information from these entities through John Doe summonses, the IRS expects to be able to identify Sovereign’s U.S. clients who may be avoiding or evading taxes.

Federal law requires U.S. taxpayers to pay taxes on all income earned worldwide. U.S. taxpayers must also report foreign financial accounts if the total value of the accounts exceeds $10,000 at any time during the calendar year. Willful failure to report a foreign account can result in a fine of up to 50 percent of the amount in the account at the time of the violation.

Lotus Elise S Cup is Just Around the Corner

Returning to its race-bred ethos, Lotus has completed the development of the Elise Cup R into an enticing new model - the road legal Elise S Cup.

Following extensive testing, Lotus has honed the ever-popular Elise S into a Cup variant. Visual appeal has been bolstered with the striking addition of a front splitter, with end winglets, lateral bargeboards, a fixed roof, tail wing and a purposeful rear diffuser.

These combined aerodynamic benefits increase downforce to a staggering 66kg at 100mph and 125kg at the 140mph top speed. This improved grip in the corners leads to a dramatic 3 second reduction in lap time at the Lotus test track.

Put into perspective, this 66kg downforce at 100mph would equate to a stack of £1 coins over 21 metres high, compared to a measly 1.66 metre stack generated by the regular Elise S at the same speed.

The equivalent weight in 24 carat gold bullion would add up to £1.5m, but this isn't reflected in the price, with UK cars starting at just £43,500.

The 'fresh out of the box' appeal, allied to Lotus's attention to detail, means that the Elise S Cup can be driven back from work on Friday and raced on Saturday, such is its dual-nature character. To create the transition from road to thoroughly focussed track car, the Elise S Cup is equipped with a competition specification roll-hoop, which also provides fixing points for competition safety harnesses.

The first Elise S Cups will be coming off the line and onto the road (and track) at the start of January. Orders can be placed now:

BIZweek Edition 26 – Samedi 20 Décembre 2014

Élections Générales - Le secteur privé et l’Alliance Ptr-MMM

Offshore - Les Défis du ‘Global Business’

Biz Alert - Un Jackpot de Rs 4,5 Millions pour Callikan

Un Chairman ‘Roder Gro Bout’

Turbulences à la BOM

Un Chairman ‘Roder Gro Bout’

Turbulences à la BOM

18 December 2014

Offshore Pilot Quarterly (December 2014, Volume 17 Number 4)

Dwarfs and Dictators

I wrote about Brazil’s criticism of Israel’s actions against Palestinians when hostilities broke out between them in July of this year in my September Private Client Adviser blog (“Small Talk”) and I mentioned how Brazil thought that the force used was “disproportionate”. Israel’s response to the use of that adjective was to describe South America’s largest country as “a diplomatic dwarf”. Politics and countries aside it would not surprise me if that adjective is increasingly applied well beyond the Middle East - and not diplomatically – as the fine mess that is the transparency policy now espoused by developed nations progresses. Hopefully its shelf life will not be too long (“the elephant in the room” has, thankfully, almost left it, as has the 800-pound gorilla), but meanwhile we still have people “reaching out” to us; we’re told about “the prism of opportunity” and those who like “crystal balling”; presently there is a rash of references to “pivotal” by both politicians and businessmen (I only hope that the rash will clear up quickly). It is much like the tendency to avoid original thought and substitute trite words and phrases, condemned by George Orwell in his essay “Politics and the English Language” when he wrote about “gumming together long strips of words which have already been set in order by someone else, and making the results presentable by sheer humbug”.

On the issue of humbug, members of Britain’s House of Lords have fallen foul of the heightened due diligence now being applied by banks in relation to their customers. Cries of being treated like “deposed dictators or political pariahs” have echoed in the second chamber of Parliament in the Palace of Westminster. Treasury Minister Lord Deighton has said that when members try to open accounts the banks, in relation to due diligence, were acting “disproportionately” in their case. Currently, the parliamentarians are not classed as politically dependent persons – although new emerging global standards will change all that. Lord Deighton referred to box-ticking exercises on the part of the banks; but this robotic approach, devoid of judgement, is not confined to Britain nor banking.

It is regrettable but true that when applying due diligence procedures, most compliance departments – connected with banking or not – bounce their thoughts no further than the boundaries of the polyhedron on the page before them; venturing beyond and allowing common sense to intrude is a no-go area. 2015 is the Year of the Sheep in China; they’ve been bleating in compliance departments for years now. Quantitative easing is one thing; bankers appear to have embarked on a staff qualitative easing programme years ago.

This failure to exercise judgement has only added to the burden of conducting business which is already stifled with ever-lengthening lists of requirements to comply with tax, terrorism and transparency policies. And whilst a whole compliance industry has been created to address these concerns, it is not too indelicate to ask: what is the general level of skill of those enforcing the rules? You can tell me of his or her academic degree; but first tell me about his or her degree of experience.

Last month celebrations took place in Germany as it was the 25th anniversary of the fall of the Berlin Wall; that same month leaders representing 85 per cent of the world’s gross domestic product, 75 per cent of the world’s trade, and 65 per cent of the world’s population gathered in Brisbane, Australia. This mix of 20 of the world’s largest, advanced and emerging economies, collectively known as the G20, want to “knock down the walls of corporate secrecy” spurred on by the drive in Europe towards public disclosure of the most sensitive information about companies, trusts and foundations.

But no serious thought, however, has been given to the unintended, and damaging, consequences this can bring. Certainly, some of the G20 leaders live in countries where such steps would especially expose people to extortion, kidnapping and perhaps death; citizens in at least 8 of those countries are, in my view, particularly vulnerable. The British prime minister says that “the more eyes that look at this information, the more accurate it will be”. And I say the more dangerous it will be as well.

The Bermuda Angle vs. Triangle

Can you really envisage the United States of America falling into line with such ideas? Bermuda has told the British prime minister that when Britain, the US and Canada introduce a public register it will follow suit; the Atlantic island is the richest British overseas territory and I happen to think that it’s on safe ground with this argument. But I expect the end result will be a patchwork of truly transparent countries, enticing some business to move elsewhere. On this very point, we now see that Britain and 50 other countries that are members of the Organisation for Economic Cooperation and Development have signed an agreement on a new standard for automatic exchange of information, known as the Common Reporting Standard. But when will such reporting become common in the US, the OECD’s flag ship? The invisible man of business is still safe in Delaware which earns more than US$860 million in revenue from corporate filings and taxes that provide an estimated 25 per cent of its budget.

I understand the need to be able to determine and deter criminal activity in all its various forms; it is just the methods by which this is to be achieved that I question. Revealing tax evaders is right, but what costs should be brought to bear on the finance industry? America’s FATCA, familiar immediately by its acronym, has caused utter confusion and still the ground hasn’t settled under it. Industry leaders have reminded the US Congress and the Executive Branch that it is not for the private sector to assume the role of tax police: this outsourcing is outrageous.

The latest to complain has been the Securities Industry and Financial Markets Association which is a US industry trade group representing securities firms, banks, and asset management companies, all of which object to being “required to step into the shoes of the government” by assuming a reporting, collection and enforcement role. A survey by SIFMA shows that financial firms have spent more than US$1 billion during 2013 and (so far) 2014 on compliance efforts. It points out that this is only a fraction of worldwide expenditure by non-US entities (mainly banks). By one estimate this suggests that the final cost of the exercise could reach tens of billions of US dollars, which would be not far off the US Internal Revenue Service’s current US$11 billion annual budget. According to Economia, the British Chartered Accountants publication, a survey has shown that over half of financial organisations believe they will exceed their budget to meet the new rules under FATCA. Just under 30 per cent expect to spend between US$100,000 and US$1 million in 2015.

SIFMA also found that 67 per cent of finance executives surveyed saw the complexity of FATCA requirements as the biggest business challenge to being compliant. And just to add to the confusion for a compliance officer (who may have negligible practical knowledge of commercial operations in general), at the moment it appears that a majority of those executives involved directly in finance are uncertain as to which of their departments, and who in them, should be responsible for FATCA compliance; some thought the Chief Financial Officer (24 per cent), others the Chief Risk Officer (22 per cent) with just 13 per cent opting for the Chief Compliance Officer. But 27 per cent – the highest percentage – freely admitted that they just didn’t know who was responsible.

Now that the Republican party holds sway in the US congress and senate, it is possible that the architecture of FATCA might change. Republicans argue that the US Treasury had no authority to enter into the Inter-governmental Agreements that underpin FATCA and which are vital to its effectiveness.

Speaking of effectiveness. Does America’s IRS have the capacity to enforce FATCA? It will need a large increase in its budget and the agency has been described as being in crisis. Perhaps some 600,000 foreign financial institutions need to be recorded in a system which has had 20 hard-drives in 82 computers tracking e-mails crash; the Commissioner speaks of information technology being 15 years old, on average. Under its current budget the agency can hire only one new employee for every five it loses; the Republicans are planning to cut the budget.

Herrings and Hot Dogs

Ordinarily when one speaks of empires, ancient Rome often comes to mind as an example. Monarchs and emperors, however, are not necessarily part of them and when Winston Churchill argued that “The empires of the future are empires of the mind” I am sure he had neither of these titles in his thoughts. Certainly, empires in the strict, traditional sense were rightly thought to span centuries and yet, still, they are never permanent whatever form they may take and John Milton, the seventeenth-century English poet, rightly refers to those “hatching vain empires” in his epic poem in blank verse “Paradise Lost”. I have quoted Percy Bysshe Shelley before whose poetry underscores this, especially when he writes of the ruler Ozymandias, a mystical figure probably inspired by Egypt’s history, whose centuries-old monument is found to be slowly disintegrating:

“… Round the decay

Of that colossal Wreck, boundless and bare

The lone and level sands stretch far away.”

The Byzantine empire survived for 1,123 years against which Britain’s former empire pales into insignificance and which puts into focus, by comparison, the relative fleeting presence of today’s solitary superpower which some argue bears a close resemblance, if only in influence and strength, to an empire of old. One last example can even put Byzantium in its place: Shelley’s Egypt. The pharaohs ruled for nearly 3000 years. When Cleopatra VII committed suicide in Alexandria in 30 BC, Tutankhamun (some of whose magnificent treasures I have seen in Cairo’s museum) had already been dead 13 centuries.

By the end of the last century the description “empire” was a derogatory word – historically, it had always been one for the US – and French writers in the 1960s, in Churchillian terms, wrote of a new American empire seeking cerebral, rather than physical, conquest through cultural subversion and not arms, with the aid of Hollywood films. In 1950 Walter Wanger, the producer of Stagecoach, a western film classic, described Hollywood as a “celluloid Athens” carrying American values across a world that he believed was not even aware of it. About this time, of course, Britain was dealing with the remnants of its empire (see my November Latin Letter column “Crumbling Empires and Dreams”), and as long ago as the 1930s George Orwell had written that if Britain lost its empire the end result would be “a cold and unimportant island where we would all have to work very hard and live mainly on herrings and potatoes.”

Hollywood has had free rein in projecting American ideology on screens across the western world and shaping, to a very large degree, political thinking along the way. Celluloid has also been wonderful for perpetuating national myths. English national identity, for instance, was created mainly by the endless conflicts with the French and the triumphs of brave Englishmen; less highlighted is the fact that the Hundred Years War ended in triumph for the French with the loss of English control of royal lands in France. During Scotland’s recent referendum on independence, nationalists used inaccurate former Hollywood blockbusters about Scotland to substitute for proper historical fact. Kilts and claymores substituted for substance.

Are we about to see the rise of the Chinese eastern, as opposed to the American western? The classic role played by John Wayne was on the wane a long while ago. China’s film industry would seem to be where America’s was in the 1930s; however, where power has been in the hands of the studios in Hollywood, it is the state in China with control and it wants to project two images: one for domestic consumption and the other for export to the world; Chinese patriotism, not American, will be the emphasis. Hollywood in the past saw little difference between the two markets. Didn’t everyone want to wear a baseball cap and chew gum?

China has its own idea of what it wants to plant in everybody’s mind and it is well on the way to having the economic clout to make its mark. It has the largest film studio in the world and in 2013 it replaced Japan to become the number two film market in the world. Rob Cain, a film producer involved in co-productions between the US and China, expects the latter to have 60,000 domestic screens in 10 to 15 years.

In 1823 the Monroe Doctrine was a cornerstone of US foreign policy towards Latin American countries. It declared that any further efforts by European nations to interfere with states in North or South America would be seen as acts of aggression that would call for US intervention. In the twentieth century there was a Marilyn Monroe Doctrine, this one in the shape of a Hollywood sex symbol (born Norma Jeane Mortenson) who also once enjoyed the ear of an American president, and who served as a symbol (one of many) of the set of beliefs America wished to saturate the world with.

Nil desperandum. Britain which lost an empire is far from being an unimportant island and the choice of food is not between herrings and potatoes, no matter how many visitors may think that the fare on menus is often dull. The American president assures us he is neither a king nor an emperor, but whether you construe his country as an empire or not, America will retain its importance too; and speaking of food, we’re a long way from spring rolls replacing hot dogs at the food counter in cinemas.

Celluloid or otherwise, however, we all know what eventually happened to ancient Athens; the curtain came down on it. Goodbye Norma Jeane; but not just yet.

Offshore Pilot Quarterly (independent writing for independent thinkers) has been published since 1997 by Trust Services, S. A. and is written by Derek Sambrook

FSC Mauritius issues the draft Insurance (Linked Long Term Insurance Business) Rules for consultation

In line with its policy to enhance the transparency of its rule-making process, the Financial Services Commission, Mauritius (the ‘FSC Mauritius’) is issuing the proposed Insurance (Linked Long Term Insurance Business) Rules (the “draft Rules”) for consultation and invites the views of stakeholders and the public in general thereon. The draft Rules are available at the following hyperlink: Insurance (Linked Long Term Insurance Business) Rules

The proposals made or ideas expressed in the draft Rules do not reflect the definitive stand of the FSC. The draft Rules will be reviewed in the light of the views and comments received during this consultation exercise.

Your views and comments, by email or letter, must reach the FSC Mauritius by latest 30 January 2015 and should be addressed to:

The Chief Executive

Financial Services Commission, Mauritius

Address: 54, Cybercity

Ebene, 72201

Tel: +(230) 403 7000

Fax: +(230) 467 7172

Email: consult2014@fscmauritius.org

Financial Services Commission, Mauritius

18 December 2014

15 December 2014

Setting Up a Bogus Shell Corporation Is Really Easy

Just how easy is it to set up a bogus, anonymously owned shell entity in the United States that can be used to funnel money offshore to evade taxes or finance terrorism or crime? I decided to see for myself.

13 December 2014

BIZweek Édition 25 – Samedi 13 Décembre 2014

Post-législatives 2014: Le sort des Ramgoolam Boys scellé

Kee Cheong aigri contre Ramgoolam

11 December 2014

UN: General Assembly Adopts the United Nations Convention on Transparency in Treaty-based Investor-State Arbitration

The United Nations General Assembly adopted the United Nations Convention on Transparency in Treaty-based Investor-State Arbitration ("the Convention") on 10 December 2014. The General Assembly authorized the opening for signature of the Convention at a signing ceremony to be held on 17 March 2015 in Port Louis, Mauritius, upon which the Convention would be open for signature.

UNCITRAL undertook work on transparency in treaty-based investor-State arbitration as from 2010, and adopted in 2013 the Rules on Transparency in Treaty-based Investor-State Arbitration ("Transparency Rules"). The Transparency Rules represent a fundamental change from the status quo of arbitrations conducted outside the public spotlight. Indeed, confidentiality is often a valued feature of commercial arbitration. However, in investor-State disputes, the arbitration involves a State and often issues of public interest, as well as taxpayer funds. Acknowledging the fundamental role of the public as a stakeholder in investor-State disputes, UNCITRAL undertook the drafting of the Transparency Rules to provide a level of transparency and accessibility to the public of these disputes that is to date unprecedented. The Rules are also innovative in their approach to balancing the public interest in an arbitration involving a State, and the interest of the disputing parties in a fair and efficient resolution of their dispute.

The Convention constitutes the efficient and flexible mechanism by which the Transparency Rules will apply to disputes arising under the existing 3,000 bilateral and multilateral investment treaties currently in force. Together with the Rules on Transparency, the Convention contributes to the enhancement of transparency in treaty-based investor-State arbitration, and to the dissemination of knowledge about peaceful dispute resolution proceedings - which affect critical public sectors such as health, water and sanitation, transportation and agriculture - thereby engaging and empowering individuals and communities directly affected by them.

09 December 2014

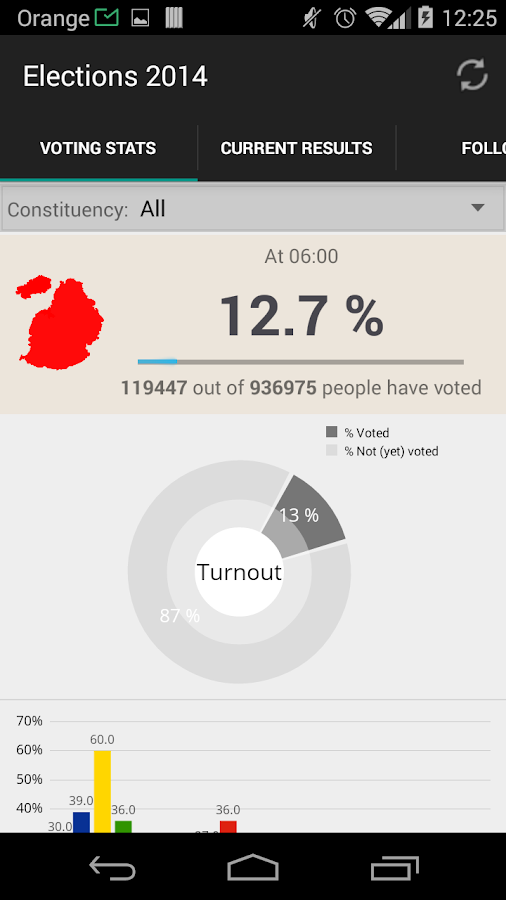

Mauritius: General Elections 2014 App

#Elections2014 app is available on:

1. Google Play for Android https://play.google.com/store/apps/details?id=eax.com.election2014

or search Elections 2014 Mauritius on Google Play

2. Web app http://elections2014.orange.mu/

(web and mobile)

As from tomorrow, this free app lets you view real-time stats as voting progresses as well as detailed results on the counting day.

Other features of Elections 2014 app:

- View the leading candidates by constituency

- Follow your favourite candidates

- View seats allocation to Parties/Independent candidates

Elections 2014 app is brought to you by the Electoral Commissioner's Office and Orange

FSC Mauritius issues FAQ on Financial Intermediaries

FREQUENTLY ASKED QUESTIONS (‘FAQs’)

FINANCIAL INTERMEDIARIES

1. What is a Financial Intermediary?

A Financial Intermediary may be broadly defined as an entity that acts as a middleman between two parties in a financial transaction. Financial intermediaries offer a range of benefits to the average consumer including safety, liquidity and economies of scale and they encompass a wide range of entities in terms of size and scale of operation.

2. Who will the FSC Mauritius consider as Financial Intermediary?

The different types of financial intermediaries that fall under the purview of the FSC Mauritius are provided under the Securities Act 2005 (SA), the Insurance Act 2005 (IA) and the Financial Services Act 2007 (FSA) (together ‘the relevant Acts’). In this respect, financial intermediaries are required to seek the required licence under the relevant Acts.

3. Who is a financial intermediary under the Securities Act 2005?

Pursuant to Section 31 of the SA, any person who proposes to solicit another person to enter into securities transactions is required to seek an investment dealer or investment adviser licence under Section 29 and 30 of the SA, respectively.

Solicitation implies to induce another person: to buy, sell or exchange securities; or to participate in transactions involving securities; or to offer persons services, recommendations or advice for those purposes.

4. Who is a financial intermediary under the Insurance Act 2005?

Any person who proposes to initiate/arrange insurance business or solicits proposal for insurance products is required to seek the relevant licence under the IA. The IA provides for three (3) categories of insurance intermediaries namely: Insurance Agent, Insurance Salesperson and Insurance Broker.

As provided under Section 2 of the IA, Insurance Agent and Insurance Salesperson are intermediaries who act on behalf of an insurer duly licensed by the FSC Mauritius and an Insurance Broker is an intermediary who acts on behalf of policyholders.

5. Who is a financial intermediary under the Financial Services Act 2007?

The Second Schedule of the FSA provides for the different categories of financial intermediaries including but not limited to Distribution of Financial Products.

6. Can a holder of a Distribution of Financial Product Licence distribute a financial product having an insurance component?

No, where a company is distributing a financial product which has an insurance component, the company is required to seek the relevant licence under the IA.

7. What happens if a company operates a financial intermediary business that falls outside the scope of the SA, IA and FSA?

No person shall carry out, or hold himself as carrying out, in Mauritius any financial services without a licence issued by the Commission.

Moreover, as per its statutory powers, the Commission may carry out a special investigation where a person has carried out, is carrying or is likely to carry out an activity which may cause prejudice to the soundness and stability of the financial system of Mauritius or to the reputation of Mauritius.

Financial Services Commission, Mauritius

09 December 2014

05 December 2014

ALFI clarification on the position of luxembourg domiciled funds in relation to the recent discussion on tax practices in luxembourg

ALFI, the Association of the Luxembourg Fund Industry, considers it important to clarify the position of Luxembourg-domiciled funds in relation to the recent discussions on the so-called “LuxLeaks”.

Luxembourg is a leading investment fund domicile with more than 3900 regulated funds, or close to 14000 fund units, currently domiciled in the Grand Duchy. Fund promoters from all over the world choose to domicile their funds in Luxembourg because of the professional expertise, the market infrastructure, a state-of-the-art legal framework, and the quality of services available in Luxembourg. Last but not least, Luxembourg plays a key role in enabling fund management companies to distribute their funds in more than 70 countries globally. Over the past 25 years, assets under management by regulated Luxembourg investment funds have grown to reach over 3000 billion EUR at the end of 2014.

ALFI, the Association of the Luxembourg Fund Industry, considers it important to clarify the position of Luxembourg-domiciled funds in relation to the recent discussions on the so-called “LuxLeaks”.

- Luxembourg-domiciled investment funds are subject to an annual subscription tax (“taxe d’abonnement”) calculated on their assets under management. In contrast, the vast majority of other countries do not apply any taxation at all on a fund level.

- The quasi-totality of Luxembourg investment funds, and more specifically ‘UCITS’ funds, do not need, nor do they obtain, rulings.

- At times, real estate or private equity funds, which represent only a few tens of billions of the EUR 3000 billion of total assets under management by Luxembourg funds, need to use ‘special purpose vehicles’ (SPV) at the level of which rulings may be granted. SPVs are common market practice and used in many jurisdictions, primarily for legal and regulatory reasons[1]. Rulings applied to SPVs mainly aim to ensure that fiscal neutrality is maintained. In other words, an investor should not be fiscally disadvantaged when he invests in real estate or private equity through a foreign fund rather than directly.

Camille Thommes, Director General of the Association of the Luxembourg Fund Industry (ALFI), says: “There is no tax advantage by domiciling an investment fund in Luxembourg. Fund managers and international investors select Luxembourg as a domicile because of the track record and unequalled expertise of the investment fund industry in Luxembourg.”

He adds: “Regulated investment funds are an important source of funding for the economy, i.e. for small- and medium, as well as for multinational companies, for infrastructure projects, environmental or social entrepreneurs. They are well-regulated financial products for investors around the world. There is no reason to draw such investment funds into the recent discussion on tax practices in Luxembourg.”

Camille Thommes emphasizes that: “Investment funds play no role in enabling people or companies to avoid tax: investors in Luxembourg investment funds will be essentially taxed in their home country, according to the local tax rules, on the income derived from their investment.”

Camille Thommes concludes: “In the meantime, everybody knows that tax rulings are legal and commonly used in many jurisdictions. They are not a “Luxembourg-specific” practice, contrary to what the LuxLeaks press seems to suggest. It is difficult to get rid of the feeling that LuxLeaks is a targeted campaign against Luxembourg”.

03 December 2014

The Law Firm That Works with Oligarchs, Money Launderers, and Dictators

If shell companies can be said to be getaway cars for bank robbers, then Mossack Fonseca may be the world's shadiest car dealership.

US: SEC Charges California Resident with Fraudulent Sales of Stock

The Securities and Exchange Commission today charged the owner of several now-defunct investment entities with fraudulently selling shares of stock that he claimed to own when he had actually purchased them for others a few years before.

The SEC alleges that Vinay Kumar Nevatia, who used several aliases while living in Palo Alto, Calif., sold approximately $900,000 worth of stock he supposedly owned in a privately-held information technology company called CSS Corp. Technologies (Mauritius) Limited. He deceived the buyers into believing that he owned the shares, orchestrated a series of secret wire transfers, and induced the stock transfer agent into recording his fraudulent sales. He stole the money he received from investors for his own use.

According to the SEC's complaint filed in federal district court in San Francisco, Kumar provided the true owners of the shares with fake updates on their investments for more than a year after he had disposed of their stock in these subsequent sales in 2011 and 2012. The actual owners had bought the CSS stock through Kumar in 2008. Kumar has never been registered with the SEC nor licensed to trade securities.

The SEC's complaint charges Kumar with violating Sections 17(a)(1), (a)(2), and (a)(3) of the Securities Act of 1933 as well as Section 10(b) of the Securities Exchange Act of 1934 and Rule 10b-5 thereunder, and seeks permanent injunctions, the return of ill-gotten gains, and a financial penalty.

The SEC's investigation was conducted by William T. Salzmann, Jason H. Lee, and Cary S. Robnett of the San Francisco Regional Office with assistance from Kristin A. Snyder, Stephanie A. Wilson, Edward G. Haddad, Brian Applegate, Michael A. Tomars, and Tracey A. Bonner of the San Francisco office's examination program. Mr. Salzmann and Mr. Lee will lead the SEC's litigation. The SEC appreciates the assistance of the U.S. Attorney's Office for the Northern District of California, the Federal Bureau of Investigation, and the Financial Industry Regulatory Authority.

FSC Mauritius issues Circular Letter on Submission of Audited Financial Statements

CIRCULAR LETTER

CL021214

02 December 2014

The Directors

Management Companies

Dear Sir/Madam

SUBMISSION OF AUDITED FINANCIAL STATEMENTS

- We refer to the Circular Letter (Ref: CL16042010) issued by the Financial Services Commission (the "Commission") on 16 April 2010 in relation to the "Submission of Audited Accounts" by companies holding a Category 1 Global Business ("GBC1") Licence.

- Following amendments to the South African Companies Act, entities in South Africa are required to use the International Financial Reporting Standards ("IFRS"). The South Africa Generally Accepted Accounting Principles ("SA GAAP") was therefore withdrawn for financial years commencing on or after 01 December 2012.

- In this respect, audited financial statements prepared in line with the SA GAAP will no longer be accepted by the Commission. A company holding a GBC1 Licence, may, without the prior approval of the Commission, prepare its audited financial statements in accordance with the following internationally recognised accounting standards: a) UK GAAP; b) US GAAP; and c) Singaporean GAAP.

- You are reminded that this Circular Letter must be read in conjunction with Circular Letter (Ref: CL 16042010).

For further information, please contact the Commission on 403 7000.

Yours faithfully

C. Ah-Hen

Chief Executive

CL021214

02 December 2014

Offshore Investment (December 2014 / January 2015): “LuxLeaks” and the “Road to Serfdom” – but watch out Romania!

Some readers of this Journal may have inadvertently overlooked the following piece of news: A group of unscrupulous journalists abusively published a set of stolen confidential documents containing correspondence between the revenue authorities of a sovereign state and some of its taxpayers such unauthorised publication was accompanied by defamatory statements about the administration and the companies concerned. Most likely, a number of readers have come across a slightly different representation of the same facts: the International Consortium of Investigative Journalists successfully unveiled the “sweetheart tax deals” granted by the Luxembourg tax authorities to several multinational companies, allowing them to unduly reduce their overall global tax bill

30 November 2014

IFC Review - Impact of the G20 BEPS Project

Richard Collier and Philip Greenfield examine how the effect the OECD and G20 BEPS project has had on the international tax environment.

Richard Collier, Tax Partner and Philip Greenfield, Tax Expert , Global Tax Policy, PWC

IFC Review - Incorporation in Offshore Centres: Naughty or Nice

Warren Bailey and Edith Liu examine firms that select a particular legal, regulatory, and disclosure environment by incorporating in an offshore financial center and the implications this decision has on a business and for its shareholders.

Warren Bailey, Professor of Finance, Samuel Curtis Johnson Graduate School of Management, Cornell University, and Edith Liu, Assistant Professor, Charles H Dyson School of Applied Economics and Management, Cornell University

29 November 2014

BIZweek Edition 23 – Samedi 29 Novembre 2014

Ponzi Schemes: En avons-nous tiré des leçons?

Vasant Bunwaree, ancien ministre des finances: «Sithanen est un bon technicien, pas forcément un bon ministre»

Biz Alert: Revoilà Ali Mansoor

Kee Cheong à la SBM?

28 November 2014

FSC Mauritius issues Circular Letter and FAQ on IFRS for SMEs

The Financial Services Commission ("FSC") issues Circular Letter and FAQ on International Financial Reporting Standards ("IFRS") for Small and Medium Entities ("SMEs")

27 November 2014

UK: Feasibility Study for the Resettlement of the British Indian Ocean Territory (draft report)

Publication of independent draft feasibility study on resettlement of the British Indian Ocean Territory (BIOT) by its former inhabitants. KPMG were appointed as independent consultants commissioned to carry out this study. Today KPMG will publish its draft final report in full.

In line with its Terms of Reference, the Feasibility Study has examined the full range of options for resettlement on each of the islands of the Territory, including Diego Garcia with its vital military base. Final views are now sought from the Chagossian community and all those with an interest. The study will conclude and issue its final report to Ministers in January 2015.

Infotech 2014: Mauritius reckoned as right ICT investment destination

Mauritius is now reckoned as the right ICT investment destination and outsourcing location and has successfully attracted key ICT players of international repute to do business on the island, the Minister of Information and Communication Technology, Mr Tassarajen Pillay Chedumbrum, said at the opening of the 21st edition of Infotech last night at the Swami Vivekananda International Convention Centre, in Pailles.

Infotech 2014, extending over four days, brings together 32 operators in the ICT sector to showcase their technology and ICT products and services. The 61 stands booked are expected to attract over 100,000 visitors.

In his address, Minister Pillay Chedumbrum stressed that the development of the ICT sector is high on the agenda of Government and no effort is being spared in promoting and facilitating the development of the ICT industry. ‘Government has wisely and proactively identified Africa as an opportune pole of growth for Mauritius to tap. The Mauritius-Africa Fund has been established to provide support to local investors to invest in and export to Africa’, he pointed out.

Our ICT sector is steadily strengthening with the setting up of more state-of-the-art technology parks, the availability of outstanding telecommunication services at more competitive rates and the proper harnessing of human resources, said the Minister. He quoted latest figures indicating that the sector continues to soar with the value added rate to the economy rising by 6,6%, from Rs 19,226 million in 2012 to Rs 20,487 million in 2013.

Speaking about measures to further the development of the ICT sector specifically as regards enhanced internet connectivity, the Minister mentioned the reduction of the International Private Lease Circuits tariffs by 16 % which adds up to a total cut of 80 % since 2005. In addition, 50,000 houses will be connected to fibre cable by next year compared to 8,000 houses connected this year, he said. The fibre optic will offer a speed up to 30 Megabytes per second, among the best in the Southern Hemisphere, added Mr Pillay Chedumbrum.

Infotech 2014

Organised by the National Computer Board, Infotech is a major annual event on the ICT calendar. The aim is to create awareness on emerging technologies and facilitate commercial exchanges in the ICT sector. Entrance is free of charge.

Infotech 2014 includes the following components:

- ICT Exhibition;

- ICT Career Guidance Corner to sensitise secondary school students, school leavers, parents and the public in general on career opportunities and prospects in the ICT-BPO sector. The Career Guidance Corner will consist of two sections namely a Presentation Section and a Counselling Section;

- Cybersecurity conference to mark Computer Security Day 2014;

- Smart Home Corner to showcase ‘intelligent’ home products and appliances;

- Technopreneurship Corner, a dedicated space to allow technopreneurs increase their visibility by promoting their products/service. The aim is to promote entrepreneurship in the ICT sector.

- Gaming Zone - a modern technology-driven entertainment platform for young people as well as adults.

26 November 2014

FAC payment gateway and Travolutionary booking platform announce integration

First Atlantic Commerce (FAC), a global online payment solutions provider, and Travolutionary, a comparison and booking platform for the travel industry, today announced their affiliation and technical integration.

FAC is a Bermuda-based, feature-rich payment gateway that was established in 1998 to deliver customized and flexible online credit and debit card processing to international corporations across the globe. The company also provides card storage functionality and risk mitigation solutions to its merchants, banks and other gateways.

Travolutionary was designed to allow travel and travel related companies to access disparate travel product sources, intelligently compare, and book them. Their capabilities apply to hotels, flights and car hire products — creating a unique combination of content diversity and rate availability.

Empowering some of the leading travel companies worldwide, the cloud based Travolutionary platform has been integrated to FAC’s gateway, which means that its customers can accept online credit and debit card payments through FAC.

Max Chertkov, Commercial Director of Travolutionary said: “We are happy to add First Atlantic Commerce to our list of payment providers, which offers our customers even more choice. FAC’s merchants will be able to gain instant access to OTA, published and wholesale rates should they choose to use Travolutionary.”

“We are pleased to be working with this highly flexible comparison and booking platform”, said FAC COO, Ronnie Viera. “Travolutionary empowers some of the leading travel companies worldwide and we are happy to be part of that offering.”

FAC is based in the Latin America Caribbean Region and specializes in serving merchants and banks across the Caribbean, Panama and Bermuda as well as in Mauritius, the EU and the UK.

AFRINIC - Careers - Chief Executive Officer (CEO) [Reference: afjob-ceo2014]

AFRINIC seeks to engage a Chief Executive Officer (CEO) who will lead a team of dedicated staff, and work with the Board of Directors to execute the strategic plans of the Company. The CEO will be stationed in Ebène, Mauritius.

ABOUT THE ORGANISATION

The African Network Information Centre (AFRINIC) is the Regional Internet Registry (RIR) for Africa. It is responsible for the distribution and management of Internet number resources - IPv4, IPv6 addresses and ASN (Autonomous System Numbers) - for the African region.

AFRINIC’s mission is to provide professional and efficient distribution of Internet number resources to the African Internet community, to support Internet technology usage and infrastructure development across the continent and to strengthen Internet self-governance in Africa by facilitating and encouraging participatory policy development.

AFRINIC operations are overseen by a Board of Directors (BoD) elected by members on a regional or independent representation basis, as defined by Article 11 of its bylaws. Once appointed to the Board, each Director represents and works for the whole region and not their organisations, country or sub-region.

THE ROLE (Ebène Cyber City, Mauritius)

The details of the job and the expectations are fully described in the document “Chief Executive Officer (CEO) Role” available for download here

How to Apply

To apply you should:

- Submit a full C.V. and a personally signed cover letter that clearly documents your relevant experience in line with the appointment criteria.

- Include details of expected salary and benefits package in your cover letter.

- Please also include names, positions, organisations and telephone contact numbers for at least two references, one of who should be your current/most recent employer. If you specifically do not wish referees to be contacted without your permission, please indicate thisWe will only approach referees if you are invited to attend the final interview round and will only do so with your permission.

- Finally, please ensure that you include your mobile telephone number and email address as well as any dates when you will not be available for interview.

Please email your application to ceorole@afrinic.net with the reference afjob-ceo2014 in the subject line.

All applications must be received by 17:00 UTC Friday 19th December 2014

UK: High Court holds husband to separation agreement

In L v M [2014] EWHC 2220 (Fam), the High Court held a husband to the fundamental terms of a separation agreement despite his submissions of insufficient disclosure when the agreement was signed, lack of legal advice about the implications of the agreement and that he was no longer financially able to make the agreed payments.

Mauritius Foundation

A previous Trust E in the Channel Islands was wound up and its assets migrated to Foundation E in Mauritius. The wife made an application before Moor J for the Mauritian Foundation to be ordered to disclose the information she requested as husband said he had no control whatsoever over the Foundation which was analogous to a Liechtenstein Anstalt and claimed that he could not therefore obtain the information requested, even if he wished to do so. Moor J granted her application, and recited that it was likely that the judge hearing this case will draw adverse inferences against the husband as to his financial circumstances if this information was not provided.

Mr Bruce Blair QC (sitting as a Deputy High Court Judge):

I have said sufficient to demonstrate the fundamental duty of the Husband to assist the Court in giving chapter and verse about his precise status in and entitlement pursuant to Foundation E (previously trust) structure. It is an elementary principle of English law that the Court will look beneath and beyond the veneer and formality of trust (and analogous) structures so as to identify the extent to which their assets may properly and in reality be considered a marital financial resource. There is a plethora of authority for this proposition. It is, for example, neatly put by Lewison J in Whaley v Whaley [2012] 1 FLR 735 at 761:-

"[113] As I have said, a discretionary beneficiary has no proprietary interest in the fund. But under s 25 of the 1973 Act the court looks at resources; not just at ownership. Thus whether a beneficiary under a discretionary trust has a proprietary interest is not relevant. The resource must be one that is 'likely' to be available. This is the origin of the 'likelihood' test. No judge can make a positive finding about the future: the best that can be done is to assess likelihood. What is relevant is the likelihood of the trust fund or part of it being made available to him, either by income or capital distribution. If the husband were to ask the trustees to advance him capital, would the trustees be likely to do so: Charman v Charman [2005] EWCA Civ 1606, [2006] 2 FLR 422; A v A [2007] EWHC 99 (Fam), [2007] 2 FLR 467?. The question is not one of control of resources: it is one of access to them.

[114] In deciding that question the court must look at the facts realistically. The court will not put 'undue pressure' on trustees to exercise their discretion in a particular way, but may frame an order which affords 'judicious encouragement' to provide one spouse with the means to comply with the court's view of the justice of the case: Thomas v Thomas [1995] 2 FLR 668. The cases do not say what amounts to 'undue pressure'. But in Thomas Glidewell LJ said what would not be undue pressure (viz if:

(a) the interests of other beneficiaries would not be appreciably damaged; and

(b) the court decides that it would be reasonable for the husband to seek to persuade trustees to release more capital to enable him to make proper financial provision for his former wife).

Even if the court makes such an order the trustees are not bound to comply with the husband's request; but it is 'plainly proper for the trustees to take it into account … and commonly it will be decisive': Lewin onTrusts (Sweet & Maxwell, 18th rev edn, 2007), at para 29¬157."

As I have said, the Council of Foundation E consists of the Husband's mother and a person who may well be a figurehead Council member without a true decision-making function. The Husband could clarify such matters if he wished to do so. As Appendix A demonstrates, the Wife asserts that Foundation E holds assets possibly exceeding £20,000,000. The Husband's failure to assist the Court with regard to E is a grave omission, as Moor J. predicted it may prove to be.

25 November 2014

SGSS extends South African custody hub to Mauritius

Societe Generale Securities Services (SGSS) has extended its South African custody hub to Mauritius by becoming the first remote participant to receive approval from the Mauritius Financial Services Commission (FSC) to provide comprehensive custody services in the country.

These services will be provided in Mauritius through SGSS’ custody hub in Johannesburg, backed by dedicated teams with extensive experience and expertise in the 11 African markets in which SGSS is present.

SGSS’ pan-African integrated custody platform has been successfully connected to Mauritius’ Central Depository & Settlement Co. Ltd (CDS), the result of close cooperation between SGSS and the Mauritius regulatory authorities to amend local legislation and allow a remote custodian to participate in the market. This initiative enables SGSS to offer domestic and international investors in Mauritius first-class services that are fully compliant with international industry standards.

SGSS offers a full range of securities services in South Africa to a broad client–base of asset managers, global custodians, investment banks and broker dealers. The overall offering in the country now includes both local and global custody, clearing and settlement services across all asset classes, as well as securities lending and treasury solutions.

Extending its custody hub to Mauritius underlines SGSS’ continued commitment to sub-Saharan Africa and represents a further step in its strategy to expand its wider presence across Africa, a continent which is undergoing rapid growth, and to provide domestic and international clients with reliable and quality products and services for their operations and development.

Subscribe to:

Posts (Atom)