21 June 2018

The Angolan Sovereign Fund and the Arch-Fraudster

When historians come to write the unexpurgated story of corruption in Angola, the chapter on how dual Swiss-Angolan national Jean-Claude Bastos de Morais enriched himself from the Angolan Sovereign Fund is sure to be a page-turner.

John Christensen: Can we afford the City of London?

A secretive web of tax havens and overseas territories at the heart of British foreign policy entrenches the power of finance capitalism

Volume 25, Issue 1

Summer 2018

Pages 47-55

20 June 2018

New Panama Papers Leak Reveals Firm’s Chaotic Scramble To Identify Clients, Save Business Amid Global Fallout

The latest leak of internal documents reveals the panic that marked the beginning of the end for Mossack Fonseca.

Panama Papers: Mossack Fonseca was unable to identify company owners

A new leak of documents from the offshore service provider at the centre of the Panama Papers scandal reveals the company could not identify the owners of up to three quarters of companies it administered.

19 June 2018

Bank of Mauritius: Guideline on the issue of Commercial Papers

Commercial Paper (CP) refers to a short-term money market instrument issued by a company in the form of a promissory note. CP can be used either as a funding or as a cash management tool. Its proceeds are typically used for financing current assets or inventories, or meeting short-term liabilities. CP is seldom used as a funding vehicle for longer-term obligations.

The introduction of CP in Mauritius is expected to support the development of financial markets. CP will allow issuers to diversify their sources of short-term borrowing while investors will benefit# from a viable additional short-term financial instrument, with market-determined rates of return.

This Guideline governs the issuance of CP in Mauritius. It outlines the minimum requirements that issuers and investors should meet, the procedures to be followed for CP issuance as well as the duties and obligations of all parties involved in the process.

Tax Havens and Limited Regulation Increase Risk for Shareholders

Some large, publicly held companies are incorporated in tax haven countries, ostensibly to increase value for shareholders. But new research from North Carolina State University and the University of Arkansas finds that many such companies – particularly those headquartered in countries with limited shareholder protections – are more likely to engage in practices that benefit executives at the cost of their shareholders.

“Many of these companies are incorporated in one country – the tax haven – but headquartered in another,” says Christina Lewellen, an assistant professor of accounting at NC State and co-author of a paper on the work. “There’s long been a theory that being incorporated in a tax haven, such as the Cayman Islands, leaves a company open to theft from executives who could skim off the company’s tax savings.

“We’ve found that another key factor is the regulatory environment of the country where the company is headquartered,” Lewellen says. “Specifically, we found evidence that executives of tax haven-incorporated firms are more likely to siphon off tax savings if their companies are headquartered in so-called ‘weak governance’ countries.”

Weak governance countries, such as China, are deemed to have limited rules in place to protect shareholders.

To examine this issue, the researchers evaluated data on more than 14,000 publicly held companies. The data set included information on 1,127 companies that are incorporated in tax haven countries – of which 874 had their headquarters in weak governance countries.

One key finding was that although tax avoidance results in higher cash flows, which is generally associated with higher dividend payout, tax haven companies headquartered in weak governance countries paid an average of 83 percent less in dividends to their shareholders, as compared to other companies in weak governance countries with similar tax avoidance levels.

“That’s the opposite of what you’d expect,” Lewellen says. “Those tax haven companies should have more cash, since they pay fewer taxes – but shareholders don’t see that money. In contrast, we found that tax haven companies with headquarters in well regulated countries do pass on tax savings to their shareholders.”

The researchers also found that tax haven companies in weak governance countries do not see any benefit from the cash tax savings in terms of earnings performance. Those companies performed an average of 53 percent lower than other companies in weak governance countries with similar levels of tax avoidance.

“This tells us that the tax haven companies in weak governance countries were not investing their tax savings wisely, if at all,” Lewellen says. “And, again, tax haven companies in well regulated countries did not see this lapse in performance; their performance was comparable to their peers.

“One take-away here is that incorporating a company in a tax haven country can benefit shareholders, but is much less likely to do so if the company is headquartered in a country that doesn’t take steps to protect shareholder rights.”

The paper, “The Complementarity Between Tax Avoidance and Manager Diversion: Evidence from Tax Haven Firms,” is published in the journal Contemporary Accounting Research. The paper was co-authored by T.J. Atwood of the University of Arkansas.

The Complementarity Between Tax Avoidance and Manager Diversion: Evidence from Tax Haven Firms

We investigate whether tax avoidance and manager diversion are complementary when the costs of diversion are low by comparing dividend payouts, performance, and overinvestments of tax haven firms versus other multinational firms based in countries with weak and strong investor protections. Desai and Dharmapala (2006, 2009a, 2009b) and Desai et al. (2007) set forth a theory of tax avoidance within an agency framework (the D&D theory) based on the assumption that tax avoidance and manager diversion are complementary when the corporate governance system is “ineffective” (i.e., the manager’s expected costs of diversion are low). Studies developing the D&D theory provide indirect evidence consistent with the model’s predictions but do not directly test this complementarity assumption. Recent studies of U.S. firms find no complementarity or find evidence inconsistent with this complementarity. Tax haven firms are corporate groups whose parent firms are incorporated in tax haven countries that are not the countries where the groups’ headquarters or primary operations are located (i.e., their “base” countries). We argue that tax haven incorporation potentially lowers the costs of diversion for managers of firms based in countries with weak investor protections. Using a sample from 28 base countries, we provide evidence that manager diversion and tax avoidance are complementary for tax haven firms based in countries with weak investor protections but not for tax haven firms based in countries with strong investor protections. Our results are consistent with the complementarity assumption underlying the D&D model and provide additional insights into the potential impact of the decentralization of the global firm.

Authors: T.J. Atwood, University of Arkansas; Christina Lewellen, North Carolina State University

Published: June 12, Contemporary Accounting Research

DOI: 10.1111/1911-3846.12421

18 June 2018

GDPR: The challenges facing the tech market

The GDPR has created an avalanche of work for lawyers, and some big headaches for clients

Mauritius: Reform of Financial Services Sector enunciated in Budget 2018-2019

In light of the ever-increasing challenges faced by the Global Business sector, Government is committed to give its full support to the sector whilst ensuring compliance with the best international norms and standards, underlined the Prime Minister, Minister of Finance and Economic Development, Mr Pravind Jugnauth, in the 2018-2019 Budget speech.

To this end, a number of measures have been announced in Budget 2018-2019, namely: the introduction of a new harmonised fiscal regime for domestic and Global Business Companies and a specific fiscal regime for banks; the Financial Services Commission (FSC) will cease to issue Category 2 Global Business Companies licences as from January 2019, with a grandfathering provision for existing companies.

Moreover, Global Business Companies will be required to comply with enhanced substance conditions and a new framework to govern and improve the oversight of Management Companies will be established.

The Prime Minister also pointed out that in view of enhancing the country’s competitiveness as a financial centre, the FSC will further develop equivalence frameworks with other key jurisdictions. It will host a Regional Centre for capacity building and best practices in our mutual combat against financial malpractices in collaboration with the Organisation of Economic Cooperation and Development.

He recalled that the Blueprint announced in the 2016-2017 Budget, aiming to take the financial centre to a new level of development, has now been completed with the support of international consultants. In this context, a Steering Committee will be set up to ensure the timely and effective implementation of the recommendations of the Blueprint.

16 June 2018

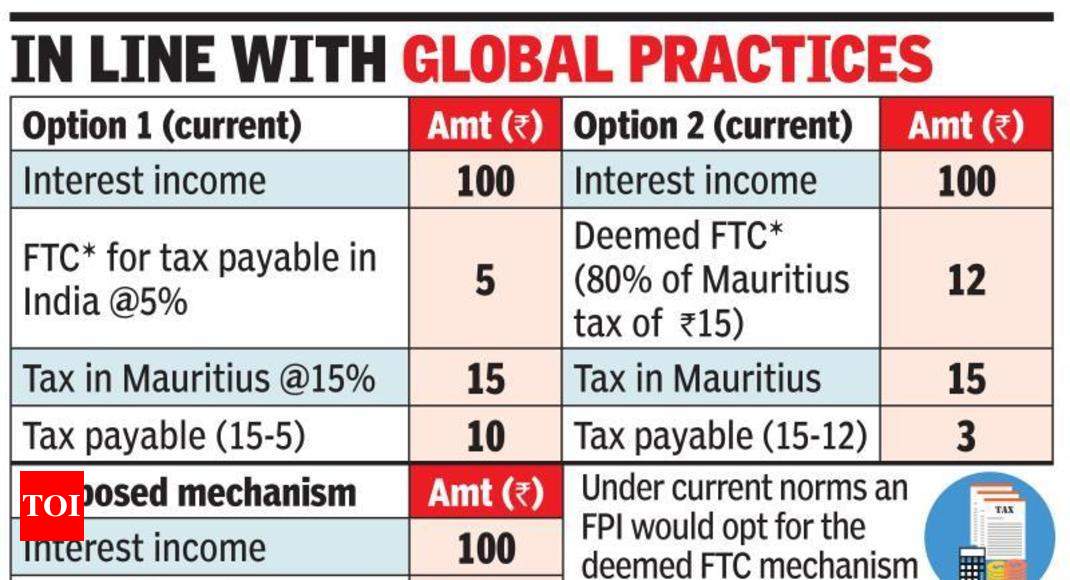

Mauritius revises tax credit rules for foreign companies

The deemed FTC mechanism, available to companies holding a category 1 Global Business Licence (GBC 1), will be abolished from 31 December 2018 and will be replaced by a partial exemption mechanism.

15 June 2018

FSC issues Communiqué: Consultation on Practice Notes for Management Companies when providing Corporate Trustee Services

The Financial Services Commission, Mauritius (the “Commission”) is considering to issue Practice Notes for Management Companies when they provide Corporate Trustee Services.

The aim of the proposed Practice Notes is to set out internationally recognised standards and good practices to ensure the sound conduct of business in the financial services sector and in the global business sector. The proposed Practice Notes are in line with the Commission’s objective to enhance the reputation of Mauritius as an International Financial Centre.

The Commission is seeking views and comments from the industry, relevant professionals and the public on the proposed Practice Notes which can be consulted here.

Your views and comments should be submitted by email no later than 22 June 2018 on fscmauritius@intnet.mu.

Financial Services Commission, Mauritius

15 June 2018

Offshore Pilot Quarterly (June 2018, Volume 21 Number 2)

In the Kingdom of the Blind

I was pleased to read that there is still a scattering of practitioners who, like me, use a fountain pen; ink in a bottle and blotting pads have fared less well, it’s true, but thank heavens innovation has not completely consigned them to history and you can still get your message across without the aid of any gadgets.

What worries me, however, is the degree of innovation to which the offshore version of the English trust has been subjected. One British law professor has commented that marketing demands was pushing the trust concept beyond its fundamentals to the extent that its very essence was being eroded. It follows, naturally, that complexity equates to costs, so lawyers gain an advantage on the principle that in the kingdom of the blind the one-eyed man is king; a general truth in this specialised branch of the law. Marketing, on the other hand, and in the case of a few international financial centres, competitive imperatives, too, are corrupting trusts to the point where the question could be asked: is this instrument really a trust? In Trumpian terms it is a case of saying one thing but meaning another which has contributed to the existence of sham trusts. We have seen the foundation uprooted and transplanted to several common-law jurisdictions. Will it suffer the same fate?

Trust practitioners like myself who have regulated the trust business, drafted trust laws, as well as administered trusts and liquidated deceased estates since record turntables were the norm – despite a resurgence due to them being discovered by a new generation – have to contend with the non-professional practitioners and salesmen (the roles are often combined) who promote APTs (the acronym can equally apply to Aggressively Promoted Trusts, as it does for Asset Protection Trusts) without fully appreciating that a real trust (where assets will no longer be controlled by the donor) is first created in the mind of the settlor and then subsequently brought to life in written form. Unlike in America, the British trust has, historically, been defined as a relationship, and not a contract, between two parties. History is the key.

At Jesus College in Oxford I have emphasised during past presentations the importance of removing (or at least reducing) complexity in financial services wherever possible. When it comes to trusts I contend that if a trained trustee has a well-rounded set of morals to aid his judgment, and a keen sense of natural justice, his decisions in times of tribulation will likely be endorsed by the courts.

The roots of the English trust, after all, reach deep into the principles of equity, although centuries before the world heard that word, Seneca the Elder had identified the meaning of equity, expressing himself in a simple but clear way: “Certain laws have not been written but they are more fixed than all the written laws”; the professional trustee understands this distinction in relation to equity and the common law. The eminent British judge, Lord Diplock, once said that the beauty of common law was that it was a maze and not a motorway; if you cannot exit the maze, however, equity is there to help because it is concerned with finding solutions in cases where legal remedies are either unavailable or would be patently unfair if applied and could cause undue hardship. One so often hears the comment that there is the law, and then there is justice; both are not the same.

Equity developed in feudal England in the King’s Chapel, which was charged with issuing official documents, such as royal writs. The post of Chancellor, a state official, by the 14th century included being a chief adviser to the King, serving as the head of the affairs of state and, as some put it, the King’s conscience. This responsibility for issuing writs for use in the royal courts sometimes made him aware of the unfairness and failings of the common law and this would lead him to grant relief to a petitioner. During the 15th century this practice had evolved into a Court of Chancery which provided judicial relief to those who had lost their way in Lord Diplock’s maze.

Plumbers and Judges

The Chancellor was guided by his moral conscience, not by law books, and indeed he did not refer to previous legal decisions or rules but followed the procedures of the ecclesiastical courts, which is not surprising, as he was not a lawyer but nearly always a senior clergyman, such as a bishop. Consequently, in the early stages of the Chancery court’s development the Chancellor did not consider that he had any judicial jurisdiction, being independent of the courts of common law. But following the appointment of Lord Nottingham as Chancellor in 1673, who set about having the principles and rules of equity translated into a system, it became the practice to appoint a prominent lawyer as Lord Chancellor. Common sense, presumably, was best left to the law courts, even if its presence was not always obvious.

Although I advocate training for your trade and preparation for your profession, there are instances where extremes arise and when judgement is bullied by bureaucracy – not to mention professional protectionism. Philosophy is a fine case in point and which only became a profession during the last few centuries. Both Socrates and Baruch Spinoza were neither professors nor tenured dons, anymore than England’s ecclesiastical courts, which applied the virtues of equity, were peopled by lawyers. The measured judgements required, however, did not necessarily need lawyers, just men who emulated Socrates and Spinoza and possessed to some degree a combination of common sense and tolerance which, together with a compassion for the human condition, infused their thought.

More recently previous presumptions on countless subjects are being questioned, if not found to be wrong. University, for example, does not offer the single, solitary path to knowledge and vocational training is a comparable alternative. After all, when the judge’s toilet malfunctions badly, it’s the tools

of the plumber and not a shelf of law books that will find the solution. Intellectual snobbery has its part to play, and it was Winston Churchill who so aptly put it when he said that he went to the university of books for his education.

Things equestrian can shine a light on such misguided presumptions. Probably, like myself, you have never had reason to consider that wild horses eat tough grass which will gradually wear down their teeth, whereas in captivity they are fed softer food and their teeth grow unchecked. Unless, however, the teeth are filed down (the process is called ‘floating’) they can grow too long and will cut the horse’s cheeks. Floating must be done by hand and it is hard work because besides needing first to calm the animal, its mouth must then be held open while its teeth are vigorously filed.

Floaters, however, are not trained veterinarians, and in the American state of Texas the State Board of Veterinary Medical Examiners outlawed them, despite the fact that very experienced floaters are tantamount to skilled artisans. The State Board, however, considers a floater as practising veterinary medicine without a license for which fines and possibly prison can be the result; the fact that veterinarians have no specialist training themselves in the field was considered immaterial. In the event, four seasoned Texan floaters filed suit – as opposed to teeth – in order to be able to continue earning a living and they won their case. Different courses for different horses. Monopolies and vested interests are not the sole domain of commerce, as I have observed.

Fiduciaries, like floaters, to my mind practise a vocation if they meet the criteria: a thorough study of the law and administration of trusts with the ability to also exercise, through practical training and teaching, an adequate degree of measured judgement in order to serve the best interests of the beneficiaries. They need neither a judge’s robes nor reasoning and rather than being the King’s conscience, they must be, at all times, the trust’s conscience.

Just before leaving London in 1979, ahead of going to the Cayman Islands (a time when offshore really meant offshore), I purchased a copy of The Modern Law of Trusts (Fourth Edition) by David B. Parker and Anthony R. Mellows. In their introduction the authors said that “since the trust was invented, no lawyer has been able to give a comprehensive service to his client without a thorough grasp of the subject”. But it follows that having a thorough grasp of trusts does not require you to be a lawyer. This realisation in the 21st century is but one of many entrenched, outmoded beliefs that are crumbling.

George Orwell and Strippers

Despite the immense contribution made by Lord Nottingham, who has been called the father of equity (I would say that Seneca the Elder is a worthy contender), what becomes clear is how important moral principles are and although Plato wanted states ruled by philosopher kings, I argue that business (especially trust companies) also requires a generous dose of wholesome philosophy. No finer example can be found than the Roman Emperor Marcus Aurelius Antoninus. His Book of Meditations is truly timeless, as is the Complete Works of Michel de Montaigne. They may have both died at 59 years of age and had lived centuries apart, but their philosophies remain as fresh as tomorrow’s morning dew.

As a devotee of fountain pens and the written word, I find that simple language, like simple offshore structures, is also under siege; the capital of convolution, as far as language (and, by extension, legal documentation) must surely be the United States of America. George Orwell, wizard of the written word, would have been horrified. Take, for example, a county ordinance in Pennsylvania which stipulates that strippers must cover one-third of their buttocks when they are dancing. The ordinance defines a posterior as being the “rear of the human body” and is “between two imaginary lines, one on each side of the body (the 'outside lines'), which outside lines are perpendicular to the ground and to the horizontal lines described above and which perpendicular outside lines pass through the outermost point(s) at which each nate meets the other side of each leg.”

No wonder there is an organisation called Plain Language Association International. But don’t despair: those needing a definition of a bare trustee rather than a buttock can contact me, although the answer won’t require me to resort to geometrical terms.

Offshore Pilot Quarterly (independent writing for independent thinkers) has been published since 1997 by Trust Services, S. A. and is written by Derek Sambrook

Mauritius Budget 2018-2019 - Reforming our Financial Services Sector

Reforming our Financial Services Sector

The Blueprint which I had announced in last year’s budget to take our financial centre to a new level of development has now been completed with the support of international consultants.

A Steering Committee will be set up at the Prime Minister’s Office to ensure the timely and effective implementation of the recommendations of the Blueprint.

In light of the ever-increasing challenges faced by the Global Business sector, Government is committed to give its full support to the global business sector whilst ensuring compliance with the best international norms and standards. The two can only go hand in hand. To this end, I am announcing the following measures:

- First, we are introducing a new harmonised fiscal regime for domestic and Global Business Companies and a specific fiscal regime for banks;

- Second, the FSC will cease to issue Category 2 Global Business Companies licences as from January 2019, with a grandfathering provision for existing companies;

- Third, Global Business Companies will be required to comply with enhanced substance conditions; and

- Fourth, we will establish a new framework to govern and improve the oversight of Management Companies.

Madam Speaker, the FSC will further develop equivalence frameworks with other key jurisdictions in view of enhancing our competitiveness as a financial centre.

And the FSC, in collaboration with the Organisation of Economic Cooperation and Development (OECD), will host a Regional Centre for capacity building and best practices in our mutual combat against financial malpractices.

Review of Taxation of Global Business Companies

The Deemed Foreign Tax Credit regime available to companies holding a Category 1 Global Business Licence will be abolished as from 31st December 2018.

A partial exemption regime will be introduced whereby 80% of specified income will be exempted from income tax. The exemption will be granted to all companies in Mauritius, except banks, and shall apply to the following income –

- foreign source dividends and profits attributable to a foreign permanent establishment;

- interest and royalties; and

- income from provision of specified financial services.

Companies licensed by the Financial Services Commission (FSC), claiming the partial exemption, will have to satisfy pre-defined substantial activities requirement of the Commission.

The existing credit system for relief of double taxation will continue to apply where partial exemption is not available.

The Category 2 global business regime will be abolished and the Income Tax Act provisions applicable to that regime will be reviewed accordingly.

The current regime will continue to apply until 30th June 2021 for companies, which have been issued a licence prior to 16th October 2017.

Taxation of Banks

The Deemed Foreign Tax Credit regime available to banks will be abolished as from 1st July 2019.

In its place, a new regime specific for banks will be introduced which will make no distinction between Segment A and Segment B income. The tax rates will be as follows –

- chargeable income up to Rs 1.5 billion will be taxed at 5 %; and

- chargeable income above Rs 1.5 billion will be taxed at 15%.

In addition, an incentive system will be introduced for banks having chargeable income exceeding Rs 1.5 billion. Under this system, any chargeable income in excess of the chargeable income for a set base year will be taxed at a reduced tax rate of 5% if pre-defined conditions are satisfied.

Special Levy on Banks

The Special Levy on Banks is currently –

- 10% of chargeable income for Segment A banking business; and

- 3.4% on book profit and 1% on operating income for Segment B banking business.

The current formula which is scheduled to end by June 2018 will be maintained up to June 2019.

The Special levy under the Income Tax Act will be removed with effect from 1st July 2019. A Special levy will be introduced under the Value Added Tax Act and will be charged on the net operating income derived by banks from its domestic operations.

Financial Services Act

The Financial Services Act will be amended to –

(i) allow the FSC to –

- give directions to any person as may be required, for the purposes of its functions, to ensure compliance with licensing conditions;

- take actions against a licensee which fails to comply with section 52 or section 52A of the Bank of Mauritius Act; and

- appoint an administrator in relation to the business activities of a person whose authorisation has been withdrawn;

(ii) ensure that licensees maintain the requirements needed for the grant of a licence at all times;

(iii) extend the scope of the offence with respect to licensees who provide false and misleading information;

(iv) extend the scope of the offence with respect to a person who destroys, falsifies, conceals or disposes of, or causes or permits the destruction, falsification, concealment or disposal of any document, information stored on a computer or other device where such information is relevant to the Commission;

(v) clarify that the Review Panel needs to receive the application for review within 21 days of the issue of the written notification;

(vi) allow for any determination of the Review Panel to be published except that any information which the Review Panel considers to be sensitive shall be omitted;

(vii) allow the FSC to regulate Custodian Services (Digital Asset) and Digital Asset Marketplace;

(viii) allow the FSC to regulate Compliance Services and Global Shared Services;

(ix) cease the issuance of Category 2 Global Business Licence as from 1st January 2019;

(x) rename the Category 1 Global Business Licence as Global Business Licence;

(xi) remove all restrictions applicable to dealings in Mauritius;

(xii) provide that all resident companies and partnerships incorporated/registered under the laws of Mauritius whose majority shareholdings/parts are held by non-resident and which conduct business mostly outside Mauritius will be required to seek a Global Business Licence or an authorisation from the FSC, through a duly appointed Management Company. The latter will be responsible for Anti-Money Laundering/Combating the Financing of Terrorism (AML/CFT), Legal, Regulatory & Corporate Governance compliance of these companies/partnerships; and

(xiii) provide for enhanced substance requirements for entities holding a Global Business Licence.

Consequential amendments will be made to sections in other legislations relating to companies holding a Category 1 or 2 Global Business Licence, namely, the Companies Act, Foundations Act, Insurance Act, Limited Liability Partnership Act, Limited Partnerships Act, Private Pension Schemes Act, Non-Citizens (Property Restriction) Act, Protected Cell Companies Act, Securities Act, and Trusts Act.

Companies Act

The Companies Act will be amended to –

(a) make provision for an offence being committed by a director for breach of duty where the director fails to disclose that he has an interest in a transaction or a proposed transaction with the company. On conviction, the Director will be liable to a fine of up to Rs 100,000 and to imprisonment for a term of up to 1 year;

(b) make provision for the Annual Report of a company to also mention any major transaction which took place during the accounting period to which it refers;

(c) provide that where the Registrar restores a company on his own motion, the requirement to give public notice in 2 daily newspapers will no longer apply to avoid unnecessary costs in relation to publication;

(d) eliminate the requirement for a certificate of current standing to contain a statement regarding payment of licence fees as same are no longer applicable;

(e) allow for disclosure and availability of Beneficial Ownership Information following enquiries related to AML/CFT;

(f) allow for the time for keeping the share register to be extended to 7 years following the removal of the company from the register;

(g) allow for enhanced protection to minority shareholders;

(h) allow for more transparency to shareholders; and

(i) allow for recovery of outstanding fees during liquidation process.

14 June 2018

IMF - Mauritius: Technical Assistance Report-Strengthening Bank Resolution and Crisis Management Framework

The Mauritius authorities have indicated their interest in formalizing and making the resolution and crisis management framework more efficient. Following extensive TA provided by Fund staff on bank resolution and crisis management, the following priorities were identified:

- Formally designate which administrative bodies are to be responsible for the resolution of individual financial institution failures, as well as for the various forms of financial and mixed groups;

- Refine the existing legal framework for early intervention and triggering resolution;

- Adopt new legal powers to support timely and effective resolution of systemically important banks;

- Issue guidance to banks to routinely prepare recovery plans for dealing with potential shocks to their capital and/or liquidity, and to review and provide feedback to banks on those plans;

- Prepare resolution plans for banks and their groups;

- Identify and remedy impediments to timely and effective resolution of banks;

- Submit Deposit Insurance Scheme (DIS) legislation to parliament;

- Adopt a formal policy framework for emergency liquidity assistance (ELA);

- Specify the role of the Financial Stability Committee (FinStab) in resolution activities; and

- Put in place cross-border cooperation arrangements with relevant foreign supervisory and resolution authorities.

Mauritius: FSC issues Investor Alert against Healy Consultants Group Plc

The FSC Mauritius hereby informs the public that Healy Consultants Group Plc is not and has not at any time been licensed by the FSC Mauritius. The FSC Mauritius therefore urges the public to exercise caution in respect of Healy Consultants Group Plc

{kind=link}

13 June 2018

The Missing Profits of Nations

By combining new macroeconomic statistics on the activities of multinational companies with the national accounts of tax havens and the world's other countries, we estimate that close to 40% of multinational profits are shifted to low-tax countries each year. Profit shifting is highest among U.S. multinationals; the tax revenue losses are highest for the European Union and developing countries. We show theoretically and empirically that in the current international tax system, tax authorities of high-tax countries do not have incentives to combat profit shifting to tax havens. They instead focus their enforcement effort on relocating profits booked in other high-tax countries—in effect stealing revenue from each other. This policy failure can explain the persistence of profit shifting to low-tax countries despite the high costs involved for high-tax countries. We provide a new cross-country database of GDP, corporate profits, trade balances, and factor shares corrected for profit shifting, showing that the global rise of the corporate capital share is significantly under-estimated.

Tørsløv, Thomas and Wier, Ludvig and Zucman, Gabriel, The Missing Profits of Nations (June 2018). NBER Working Paper No. w24701

12 June 2018

FSC Mauritius: Appointment of Mr Martin Wilding as Director of Authorisation and Supervision

The Financial Services Commission, Mauritius (the “FSC”) is pleased to announce the recent appointment of Mr Martin Wilding as Director of Authorisation and Supervision. Mr Wilding is on secondment from the Dubai Financial Services Authority (“DFSA”), the financial regulatory agency of the Dubai International Financial Centre. The FSC Mauritius and the DFSA signed, in October 2015, a Memorandum of Understanding (MoU) on capacity building and other collaboration. Both authorities, inter alia, agreed on the need to increase technical exchanges for the purpose of knowledge and better understanding of each other’s financial regulation.

Mr Wilding has over 20 years of experience in the regulatory field with specialisation in authorisation and supervision. Prior to joining the FSC, he held since 2006 the post of Director, Supervision (Authorisations) at the DFSA. While heading the Authorisation Team, Mr Wilding played a key role in developing ongoing strategy to enhance application process thereby delivering excellent results during period of significant growth in application volumes. He also participated in both prudential and conduct of business supervision of a number of firms. As a member of the Senior Management Group, he extensively contributed to strategy and policy formulation. He was, inter alia, responsible in developing the DFSA’s approach to authorising firms from the fintech sector, including crowd funding and robo-advisory firms.

Prior to his career at the DFSA, Mr Wilding was a senior member of the Management Team of the Financial Services Authority (“FSA”) in the United Kingdom (predecessor of the Financial Conduct Authority). He has assisted in the development of the FSA’s policy with regards to the streamlining of application processes; and led the Individual Authorisations, Insurance Firm Supervision and Conduct Supervision teams.

During the early stage of his career, he also managed the regional sales team of a life insurance company and was a financial adviser with the Barclays Bank.

Mr Wilding holds a BA (Hons) in History from the University of Birmingham, an LLB from the Nottingham Trent University and a post-graduate certificate in Legal Practice from the College of Law, UK. He also has a number of other qualifications in the following fields: Anti-Money Laundering, International Compliance and Financial Crime, as well as, Islamic Finance.

Financial Services Commission

12 June 2018

06 June 2018

Clamping down on offshore financial centres would not raise tax revenue

The popular account of offshore financial centres as hotbeds of tax evasion is an outdated caricature that bears little resemblance to how OFCs operate.

A new report from the Institute of Economic Affairs debunks a number of myths surrounding OFCs – or tax havens – and outlines the important economic function they play in a globalised world. Their role in facilitating individual and corporate tax planning, which is entirely legal but politically controversial, has come under the spotlight, and prevented a measured conversation about their economic role.

Clamping down on offshore centres would not raise tax revenue and preserve existing levels of investment. Instead, it would change investment flows by politicising investment decisions.

Myths surrounding OFCs:

- OFCS are not hotbeds of tax evasion – by mitigating instances of double and triple taxation, offshore centres raise aggregate investment. Their existence is also associated with better economic outcomes in the countries that surround them.

- OFCs do not adversely affect the revenue-raising ability of other countries. For example, average corporate tax revenue as a share of all taxes collected has grown slightly OECD countries since 1980.

- It is not true that OFCs levy no taxes. Their average tax revenue as a share of national income is only six percentage points lower than across the OECD.

- Many OFCs do not meet the OECD’s definition of a ‘tax haven’. They tax their residents to an extend comparable with Western countries; they are transparent with foreign tax authorities; and they comply with international tax treaties.

Key points:

- OFCs have emerged to harness the benefits of a modern financial system – diversification, risk transfers and maturity transformation – when doing business in a world of sovereign nation states.

- The recent growth in the number and size of OFCs can be explained by three developments: an increase in the stock of investable capital, new investment opportunities outside Western Europe and North America, and, crucially, the growth of tax and regulatory intervention by governments.

- As more investment capital is allocated across a diverse range of jurisdictions from investors around the world, the potential for multiple taxation increases. The role of OFCs in eliminating excessive taxation has a positive impact on investment returns which compounds over time.

- Undermining the existence of OFCs would harm investment, economic growth and international capital flows, while the promised benefits from intervention are unlikely to materialise.

Commenting on the report, Jamie Whyte, Director of Research at the Institute of Economic Affairs, said:

“Offshore financial centres are a vital part of the modern global economy. Clamping down on them would not raise tax revenue, but see investment flows being shaped less by investment opportunities and more by political factors. Too often the debate around ‘tax havens’ generates more heat than light. It’s time for a rational debate around tax policies.”

05 June 2018

IMF: Inside the World of Global Tax Havens and Offshore Banking

New research reveals that multinational firms have invested $12 trillion globally in empty corporate shells, and citizens of some financially unstable and oil-producing countries hold a disproportionately large share of the $7 trillion personal wealth stashed in tax havens.

{kind=link}

01 June 2018

Sign up for EY’s Tax News Update: Global Edition

Register for EY’s Tax News Update: Global Edition (GTNU) tool for access to free, personalized email updates on important global tax developments.

Subscribe to:

Posts (Atom)